Market Pulse: February 28, 2026

Stocks mixed in February, bonds positive

Stock markets were mixed in February. The S&P/TSX Composite Index had a strong month, driven by strong materials and energy stocks. The MSCI EAFE Index also gained ground, while U.S. stock indexes were generally weaker. Fixed income was generally stronger across the board.

Index returns as of February 28, 2026

Close | February (%) | YTD (%) | |

S&P/TSX Composite Index | 34,339.99 | 7.6 | 8.3 |

Dow Jones Industrial Average (USD) | 48,977.92 | 0.2 | 1.9 |

NASDAQ Composite Index (USD) | 22,668.21 | -3.4 | -2.5 |

S&P 500 Index (USD) | 6,878.88 | -0.9 | 0.5 |

MSCI EAFE Index (USD) | 3,179.91 | 4.5 | 9.9 |

Source: Manulife Investment Management Capital Markets Strategy Team, as of 2/28/2026

Headline-driven volatility

Recent events reinforce our view that headline‑driven market volatility will likely continue through March and beyond, especially as geopolitical tensions in the Middle East remain fluid and unpredictable. With multiple state and non‑state actors involved, it can be challenging to stay on top of every development, particularly amid such a rapidly evolving news cycle.

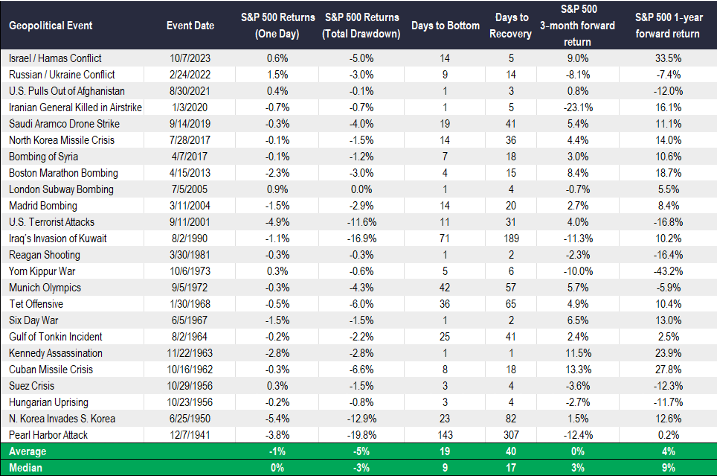

With most global geopolitical shocks, we ask ourselves if the event is disruptive or destructive. Historically, the vast majority have fallen into the disruptive category, causing temporary volatility but only limited long‑term damage to the economy or corporate earnings. Market drawdowns from such events tend to reverse once the uncertainty clears and investors refocus on fundamentals.

History shows that markets often recover quickly. Across a wide range of past geopolitical events, markets have typically experienced an initial decline, followed by a recovery that begins relatively quickly. On average, for example, the S&P 500 Index has bottomed roughly 19 days after the initial shock and has fully recovered to “break-even” levels around 40 days after the event. These patterns underscore a consistent behavioural response: investors initially reduce their risk, then re-enter the markets as clarity improves.

Short‑term reactions skew negative, but historical data shows that one‑year forward returns have often been positive, though past performance is not always indicative of future results. Over the first one to three months, markets have often exhibited heightened volatility and modestly negative performance as uncertainty peaks. However, historical data indicates that 12‑month returns following geopolitical events have often been positive, except in cases where the event coincided with—or triggered—a true fundamental shift, such as an economic recession.

In other words, markets don’t usually struggle because of geopolitical events themselves, but rather when geopolitics occasionally overlaps with macroeconomic deterioration, though this is not guaranteed.

This remains an exceptionally fluid global geopolitical environment, with dynamics often shifting by the hour. Many of the drivers behind recent market volatility are beyond any investor’s control. What is within our control—and where we place most of our focus—is ensuring that portfolios are properly structured to navigate a wide range of potential economic and market outcomes.

Geopolitical events have always had a short-term impact on the markets.

Source: Bloomberg, Manulife Investment Management, Capital Markets Strategy, as of February 28, 2026

Source: Bloomberg, Manulife Investment Management, Capital Markets Strategy, as of February 28, 2026

What can higher oil prices mean for the U.S. economy and markets?

Oil is often at the epicentre of heightened geopolitical risk, especially when the rise in risk is coming from the Middle East. Economically speaking, higher oil prices are bad news nearly across the board (but the impact has diminished over the years). It can increase costs for consumers, especially at the lower end of the income spectrum, where a greater share of spending is on gas. That said, the economic dependence on oil has diminished significantly over the years due to technological innovation (think EVs). The other element is that it can cause inflationary pressures, which then leads to higher central bank rates. The disinflation we’ve been seeing over the last several years has been helped by lower oil prices, so high oil/gas prices would likely stall further disinflationary pressures to some degree. Overall, the economic implications are relatively limited, but increased uncertainty around geopolitical risks can cause reduced sentiment. Oddly enough, U.S. consumer sentiment is already relatively negative, but market sentiment is about as positive as ever (based on valuations and equity cyclical market rotation). Ultimately, the market implications tend to be short-lived.

Monthly Lookahead

March 6 | U.S. February employment |

March 11 | U.S. February CPI |

March 13 | Canada February employment |

March 16 | Canada February CPI, housing starts |

March 18 | BoC rate announcement |

March 31 | Canada January GDP |

Important disclosures

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person.

All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients and prospects should seek professional advice for their particular situation. Neither Manulife Investments, nor any of its affiliates or representatives (collectively Manulife Investments) is providing tax, investment or legal advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investments. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investments does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Manulife Investments shall not assume any liability or responsibility for any direct or indirect loss or damage, or any other consequence of any person acting or not acting in reliance on the information contained here. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investments to any person to buy or sell any security or adopt any investment approach, and is no indication of trading intent in any fund or account managed by Manulife Investments. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investments. Past performance does not guarantee future results.

Manulife, Manulife & Stylized M Design, Stylized M Design, Manulife Wealth and Where will better take you are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates, under license.